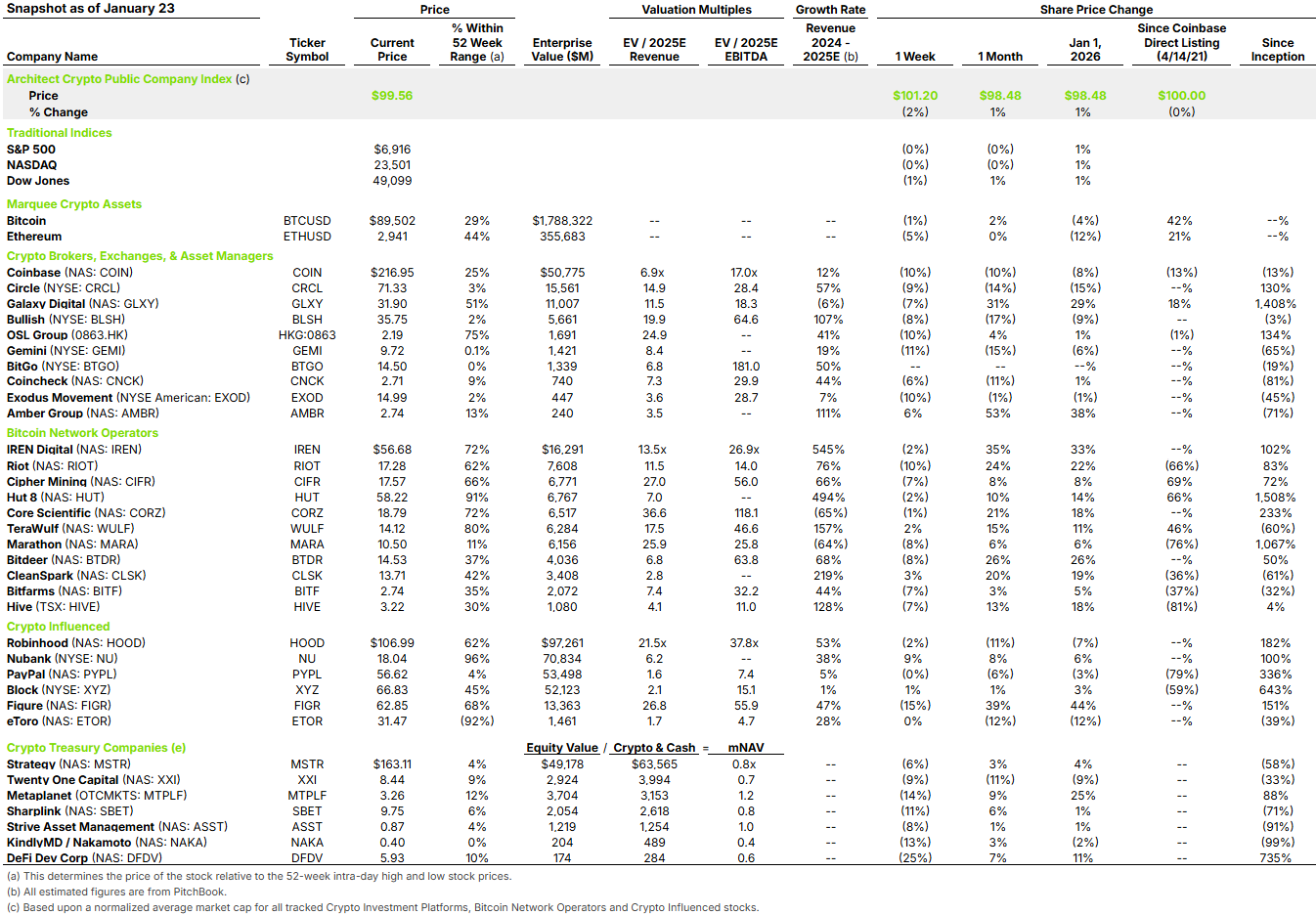

BitGo, a digital asset infrastructure company providing institutional custody and wallet services, plus a platform for trading, staking, lending, collateral management, and token and stablecoin operations. The company priced its IPO on January 22, 2026 at $18.00 per share, above its initial $15.00 to $17.00 range. The offering raised $199M of primary capital (to the company) and $14M of secondary proceeds (existing shareholders selling). The deal implied a $1.74B enterprise value, equating to 8.9x of its estimated $196M of 2025E net revenue. We define net revenue as GAAP revenue less the cost of digital asset sales, staking fees, and stablecoin sponsor fees. Reported revenue is $16B, which is not helpful from our perspective.

BitGo is the first large-scale, institutional first, crypto custodian to go public. Bullish and Gemini are exchanges whose revenues move with trading volumes and sentiment, while Circle is a stablecoin issuer that is highly sensitive to interest rates. BitGo, by contrast, sells the “picks and shovels” layer that is institutional custody and infrastructure.

More broadly, digital asset custody is a gating function for crypto’s progression. You do not get durable institutional adoption, ETFs, corporate treasuries, or large allocator participation without trusted safekeeping, strong controls, auditability, and a regulatory posture that looks familiar to traditional finance. A scaled, regulated custody platform going public helps validate custody as core market infrastructure and builds credibility for BitGo as a listed company.

Initial trading saw a high of $23.14 (+29%), but since then, the stock has fallen to $14.50 (-19% from IPO price). Gemini followed a similar pattern. It priced above its market range ($28 per share vs. $24 – $26 per share), and after an initial 2-day pop, declined before stabilizing at the initial price range. It is hard to forecast BitGo’s near-term move, but a reasonable scenario is it also stabilizes around its initial pricing range. In the end, there is a lesson for the underwriting team. Underwriters have to balance maximizing issuer proceeds with early trading optics, and in a less frothy market they should put more weight on the optics, even if it means leaving a bit more upside for aftermarket.