December 1st – December 7th

PERSPECTIVES by Eric F. Risley

Tokenized real-world assets have been a topic of discussion for a decade. As is often the case, promise and reality take quite some time to align. We remain in the promise > reality phase, although the pace of realization is certainly quickening.

The most notable tokenization success story is undoubtedly stablecoins, particularly US dollar stablecoins. Today, over $300B of these instruments are outstanding, representing about 1.2% of the US dollar money supply as measured by M2. The value proposition is simple: instant transfer of value globally in a form widely accepted as the gold standard for safety and stability, the US dollar. This has never existed before.

Figure has demonstrated strong product-market fit with tokenized home equity lines of credit (HELOCs), originating over $17B since launch in 2018. Today, Figure is initiating roughly 2% to 3% of US HELOC volume. The value proposition is more complicated and deserves a more comprehensive discussion, but, simply put, it is faster, cheaper, and more capital efficient than traditional HELOCs, with the promise of deeper secondary trading liquidity over time. Figure is by far the largest participant in the tokenized credit markets.

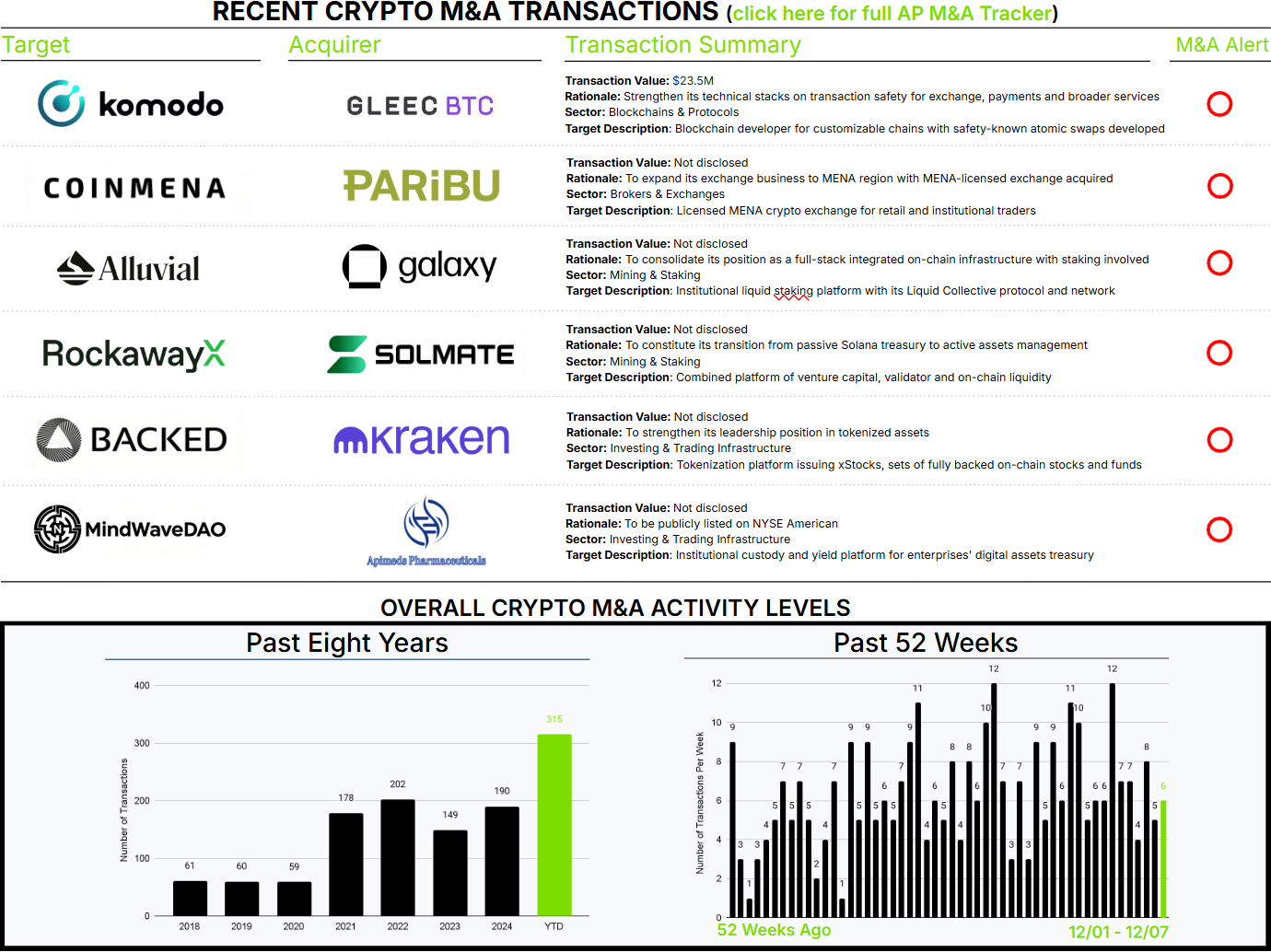

Equity is an often-discussed asset class that some feel is well suited for tokenization. This week, Kraken acquired Backed, which offers xStocks, tokens backed 1:1 by the underlying stock. The proposed value proposition is also simple: 24/7 global trading. Does this hold up to scrutiny today? Well, average trading volumes on Tesla, the most active xStock, are only 0.05% of Tesla stock volume since June 29th, 2025, demonstrating an extreme lack of liquidity. Furthermore, prices diverge slightly between these markets, with an average deviation of 0.21%.