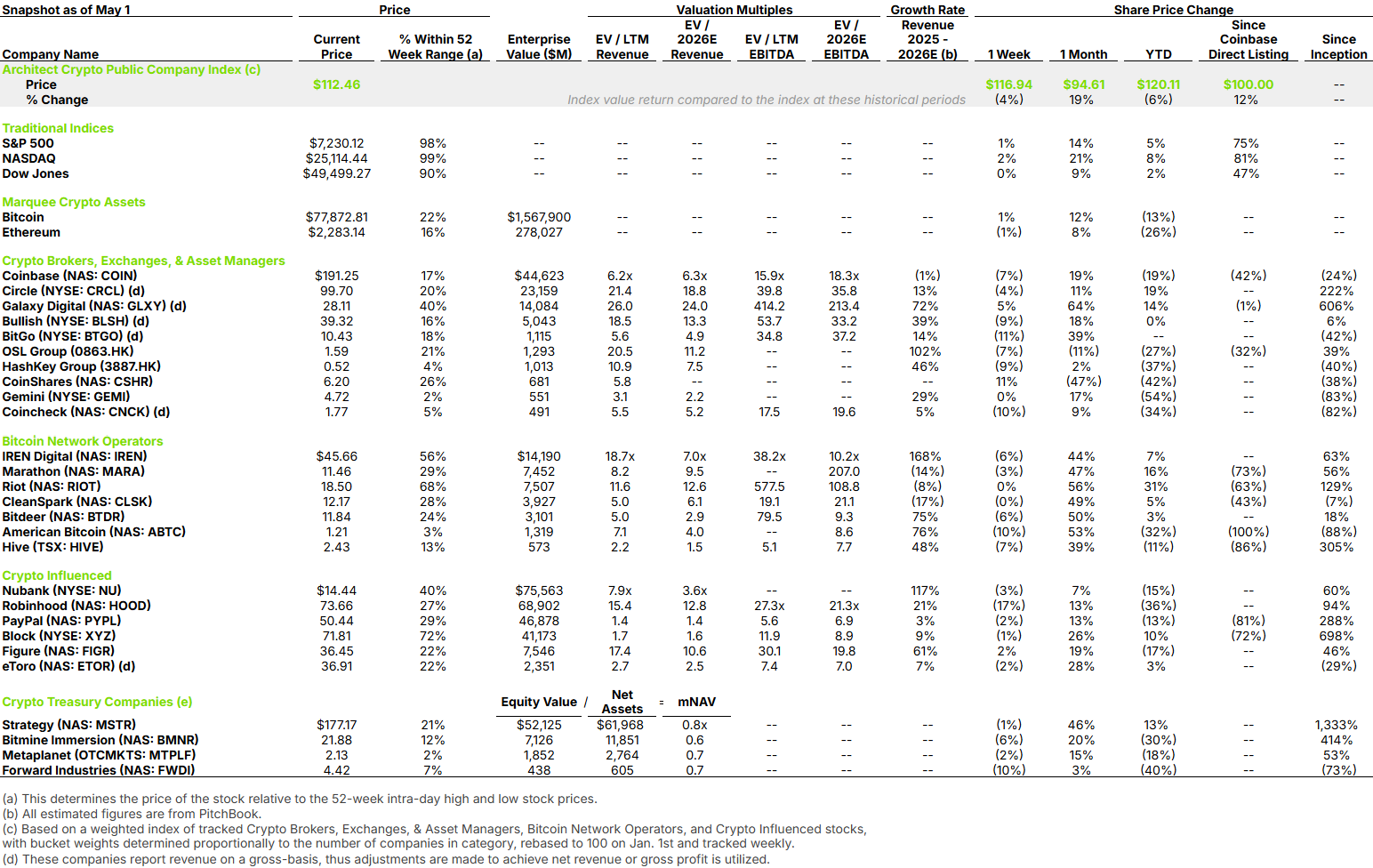

Europe Has Crypto Regulation. Where Are Its Public Crypto Champions?

Europe, particularly Switzerland, was early to regulated digital asset products (i.e. ETPs), institutional infrastructure, and a formal multi-national crypto rulebook (still pending full local implementation). Yet its largest public crypto champion, by market cap, is CoinShares, a digital asset manager with more than $6B of AUM and roughly one-third share of Europe’s crypto ETP market. Yet, CoinShares ultimately chose to transition away from Nasdaq Stockholm in favor of the U.S. Nasdaq, and today has a market capitalization of ~$500M. The next largest European public crypto assets, excluding DATs, are much smaller: Bitcoin Group SE at roughly $175M, K33 at roughly $30M, and Safello at roughly $8M.

This lack of scaled public champions is a two-part problem. First, Europe has a scarcity of risk capital relative to the U.S., resulting in only 11% as many large venture-backed enterprises as of July 2025 (OECD). Second, Europe’s public markets have structural liquidity weakness, driven by lower household allocation to financial securities, around 17% in Europe versus 43% in the U.S. (here), fragmented exchanges, and a preference for bank lending over equity financing.

Recent listing decisions make the issue tangible. In CoinShares’ Nasdaq listing announcement, the company cited access to deep institutional capital, expanded analyst coverage, and the size and liquidity of the U.S. market as reasons for transitioning away from Nasdaq Stockholm (here). Bitpanda has reportedly explored an IPO at roughly €5B, or $5.9B, while ruling out London due to liquidity concerns and opting for Frankfurt (a win for Europe) or New York (here; here).

The result is a self-reinforcing dearth of scaled public-companies. Europe’s fragmented exchanges and thinner liquidity make it harder for crypto companies to attract trading depth, analyst coverage, and institutional demand. That liquidity deficit weakens the local comparable-company set, leaving investors with fewer valuation anchors. With fewer anchors, coverage remains limited, institutions stay cautious, and liquidity stays thin, which leads to the next European crypto company having more reason to list in the U.S., sell to a U.S. buyer, or stay private.

So while Europe helped build crypto’s foundation, without the same public-market machinery as the U.S., its crypto companies have struggled to compound liquidity, capital access, coverage, and valuation into scaled public champions.