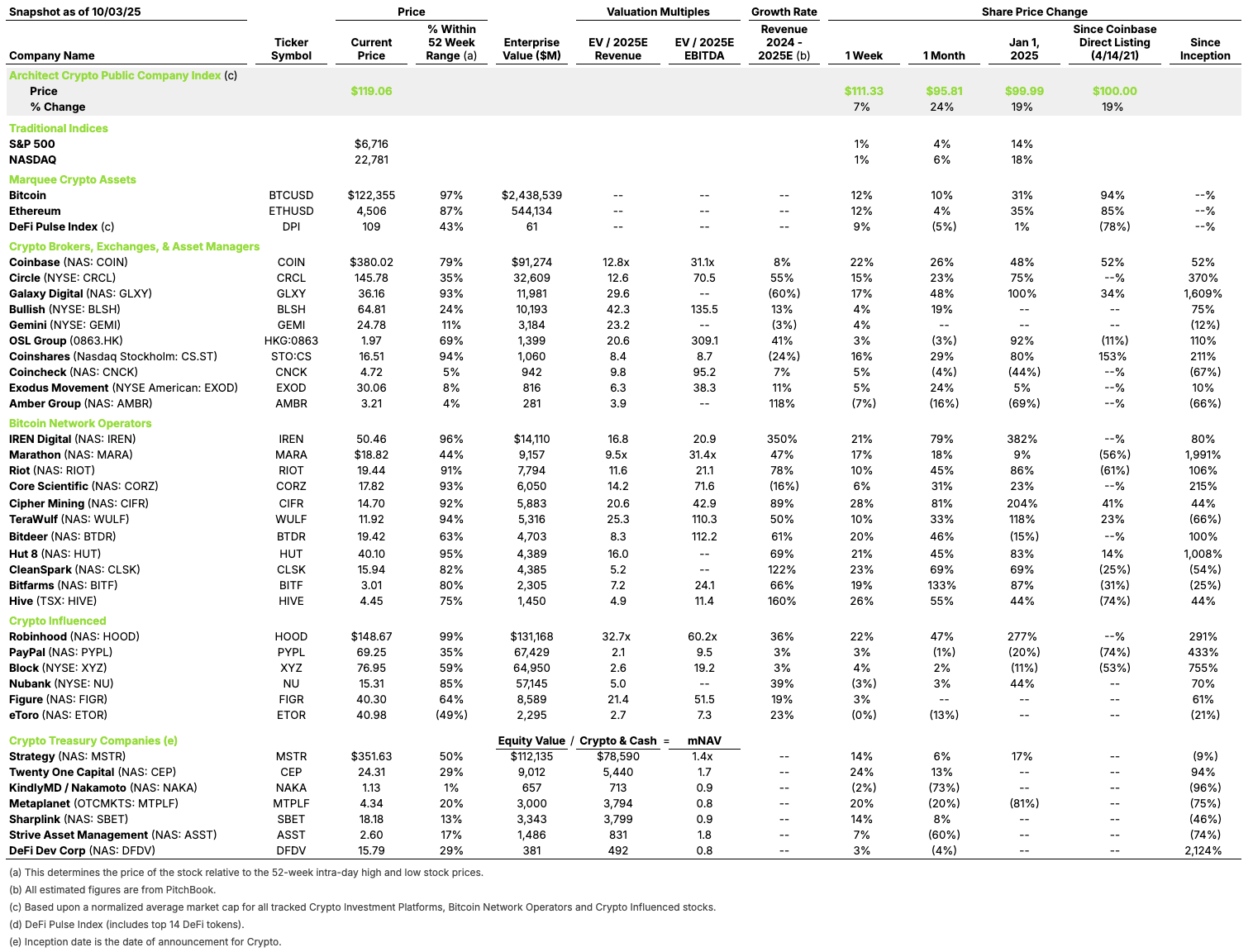

Bitcoin miners are increasingly supporting the underlying infrastructure of the AI age, with four notable announcements from our core group in the past two weeks alone. For reference:

- Cipher Mining (September 25): Won a 10-year Fluidstack AI hosting deal in Texas with a $1.4 billion Google backstop.

- TeraWulf (September 26): Seeking to raise ~$3 billion in debt to finance new data-center capacity following last month’s Fluidstack deal backed by Google.

- CleanSpark (September 25): Secured $100 million in BTC-backed credit to fund data-center/HPC build-out.

The rationale is logical. At the macro level, data-center demand is booming and is widely expected to grow rapidly over the next several years (often cited around a low-20s CAGR to a trillion-dollar-plus annual spend by decade’s end). By contrast, crypto-mining growth is typically modeled in the mid-single to low-teens percentage range, depending on assumptions for price, fees, difficulty, and power availability.

On a micro level, the unit economics of AI are more favorable because volatile mining revenue can be replaced by multi-year, contracted cash flows (lease-style $/kW-month with power pass-through and SLAs). In the AI business model, revenue density per MW is higher, margins are steadier, and miners aren’t subject to bitcoin-specific headwinds like price fluctuations, rising difficulty, and halving cycles. In short, AI colocation converts megawatts into more predictable dollars.

This recomposition of the financial profile, toward steady, predictable cash flows, enables companies to access lower-cost project financing and often earns a higher valuation multiple. Practically, investors tend to ascribe a higher multiple to contracted AI revenue and a lower, more cyclical multiple to the legacy mining slice, lifting the blended valuation as AI grows.

Finally, this transition is operationally easier than greenfield development. Miners already control the scarce inputs that AI data centers need: large power interconnects, entitled land, cooling rights, and 24/7 site operations. Critically, tenants often bring the GPUs, reducing operator capex and shortening time-to-revenue; halls can be converted to liquid-cooled, high-density layouts and energized in large chunks. This effectively makes repurposing mining campuses to AI data centers faster and cheaper than building from scratch. As such, cost-sensitive hyperscalers and AI clouds are increasingly willing to underwrite these transitions (the Google-backed Fluidstack deals at TeraWulf and Cipher are illustrative).

Given these dynamics, we expect a meaningful share of installed mining power to be reallocated to AI / HPC over the next few years (some industry estimates point to as much as ~20% by 2027). Accordingly, announcements like the ones above will be more common.