March 30 – April 05 (Published April 09th)

PERSPECTIVES by Steve Payne

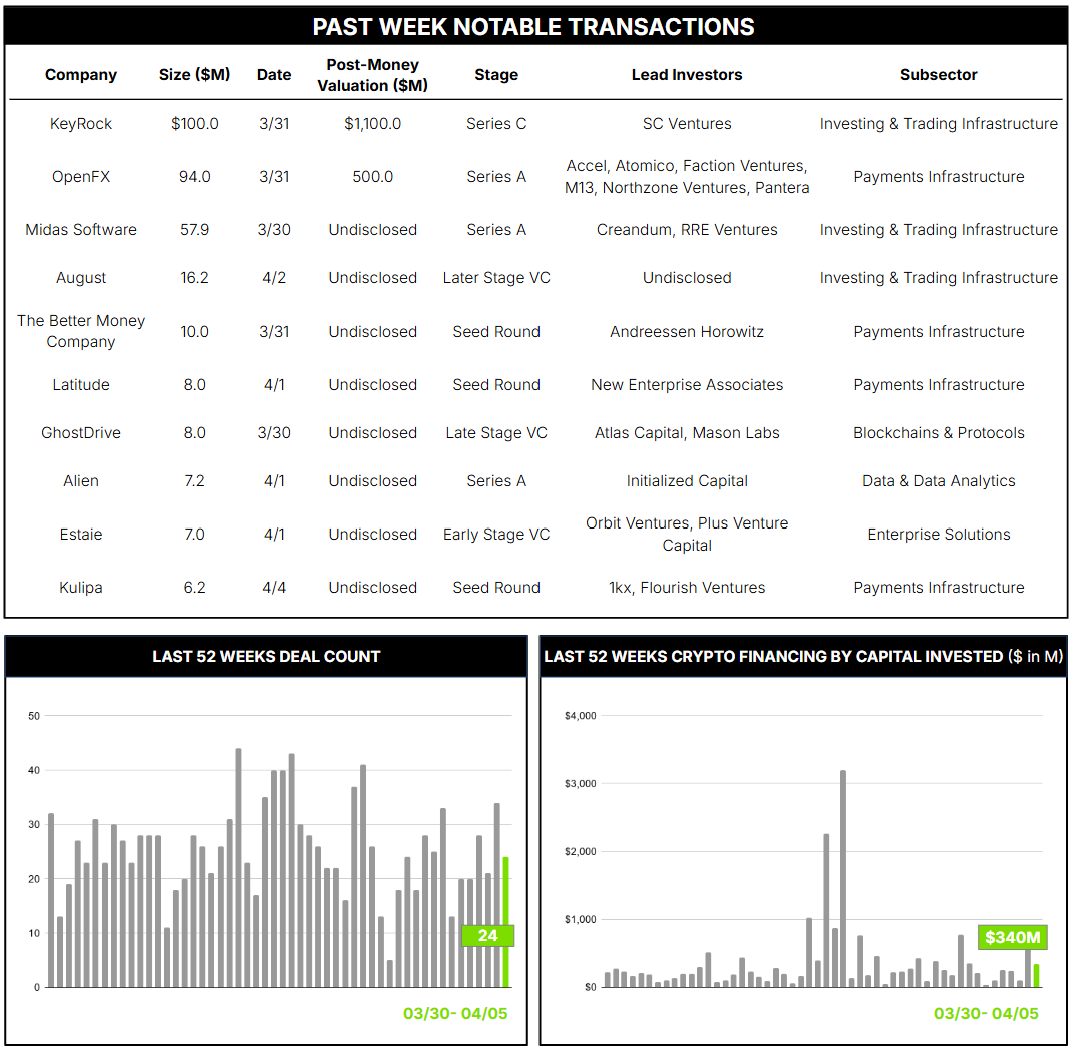

24 Crypto Private Financings Raised: $340.4M

Rolling 3-Month-Average: $303.1M

Rolling 52-Week Average: $370.6M

Announced Deals >$50M: 3

24 companies announced private funding rounds last week totaling over $340M, led by three deals that accounted for 2/3 of capital raised. A common thread: investors are backing the financial plumbing that connects crypto rails to institutional-grade markets.

Keyrock closed a Series C led by SC Ventures, Standard Chartered’s venture arm, with participation from Ripple, valuing the Brussels-based digital asset services firm at $1.1B. The round could total up to $100M and will fund balance sheet strengthening, product expansion, and M&A. Keyrock operates across more than 80 centralized and decentralized venues, offering market making, OTC, options, and, following its 2025 acquisition of Luxembourg’s Turing Capital, asset and wealth management. This is a clear unicorn-minting moment for European crypto infrastructure, backed by a tier-one banking franchise.

OpenFX raised $94M in a Series A led by Accel, Atomico, Lightspeed Faction, M13, Northzone, and Pantera, at a ~$500M valuation. Founded in 2024, the company uses stablecoins as settlement rails for cross-border FX, enabling faster and cheaper conversions for institutional clients. OpenFX now processes over $45B in annualized volume, up from $4B a year ago, with over 98% of transfers settling in under an hour. The round positions it among the best-capitalized stablecoin payments startups globally.

Midas raised $50M (bringing total funding to ~$58M) in a Series A led by RRE and Creandum, with backing from Franklin Templeton, Coinbase Ventures, and Framework Ventures. The Berlin-based platform tokenizes institutional yield strategies into compliant onchain products and will use the capital to scale its Midas Staked Liquidity system, enabling instant redemptions for tokenized assets. Franklin Templeton’s participation, itself a tokenized fund issuer, is a notable signal of institutional convergence.

The broader takeaway: capital last week flowed overwhelmingly toward regulated, institutional-facing infrastructure: liquidity provisioning, stablecoin settlement, and tokenized asset plumbing. The market seems to be rewarding companies that sit at the intersection of crypto-native technology and TradFi distribution, particularly those with demonstrable volume and regulatory footing.