February 17th – February 23rd

PERSPECTIVES by Eric F. Risley

Will stablecoins proliferate to become use-case specific?

This week, Figure announced that the Securities and Exchange Commission approved YLDS—an effective equivalent to a stablecoin. Put simply, YLDS is a traditional money market fund (a security) structured as a digital asset (token) and managed on the Provenance blockchain. Similar instruments have been issued by Hashnote (just acquired by Circle), BlackRock (BUIDL), Franklin Templeton (BENJI), and Arca (ArCoin). To date, none have scaled commercially beyond relatively modest levels. Currently, the total outstanding value of tokenized money market instruments is around $4B compared to $221B of stablecoins in their non-security form.

These securities-based stablecoins have emerged as a regulatory-compliant way to offer holders yield—a far more meaningful proposition as interest rates have risen substantially in recent years. In fact, BlackRock’s BUIDL currently offers a 4.5% APY, which is significant. Europe’s MiCA regulations prohibit traditional stablecoin issuers from offering interest, and U.S. stablecoin legislative proposals suggest that offering yield could classify such instruments as securities.

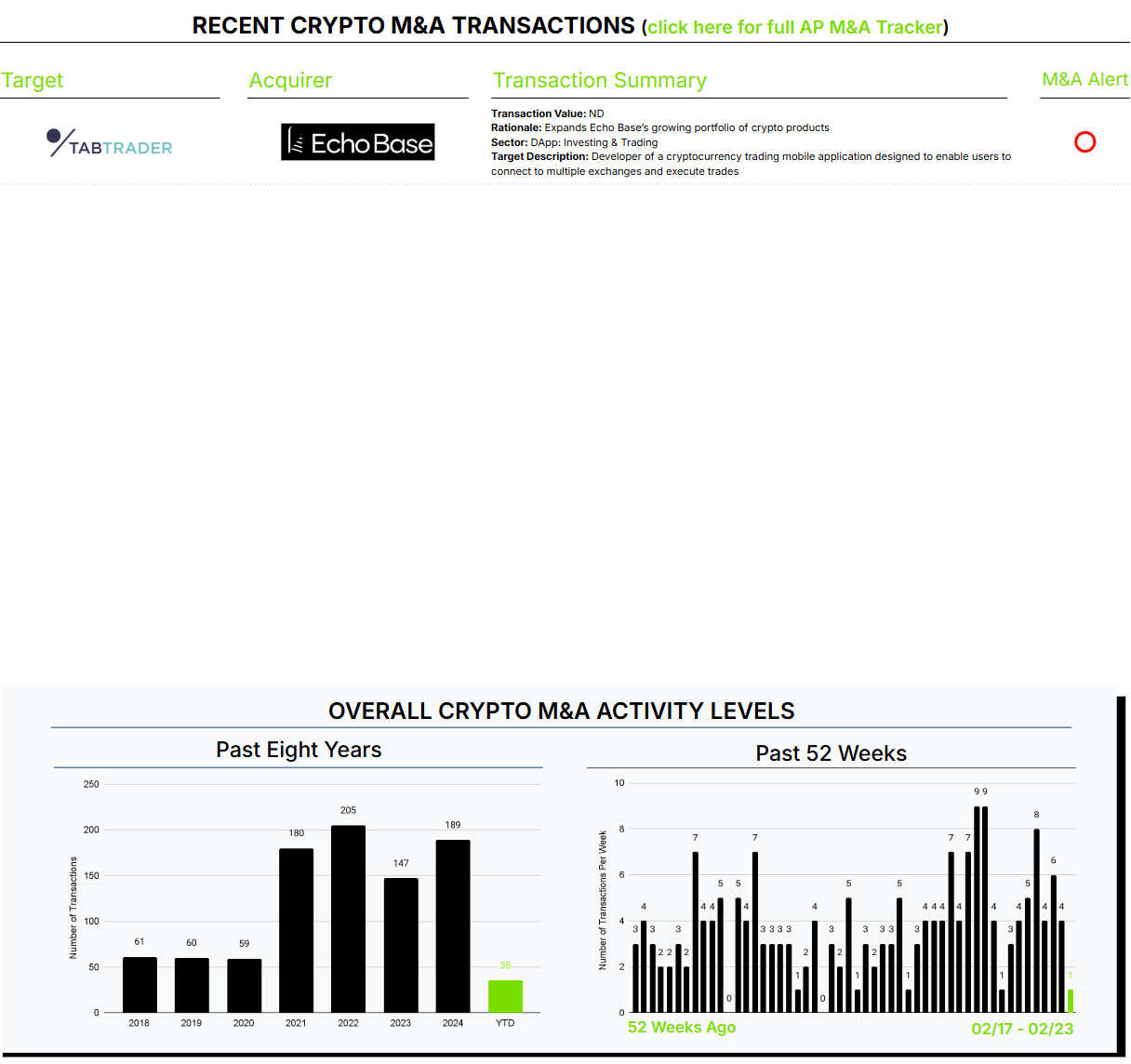

Of course, this is more complex than the simple explanation above, but one can see the risks clearly. This complexity is certainly among the motivations driving Circle’s acquisition of Hashnote (as noted in our M&A Alert) and we anticipate further strategic moves to align stablecoin value propositions with evolving regulatory requirements.