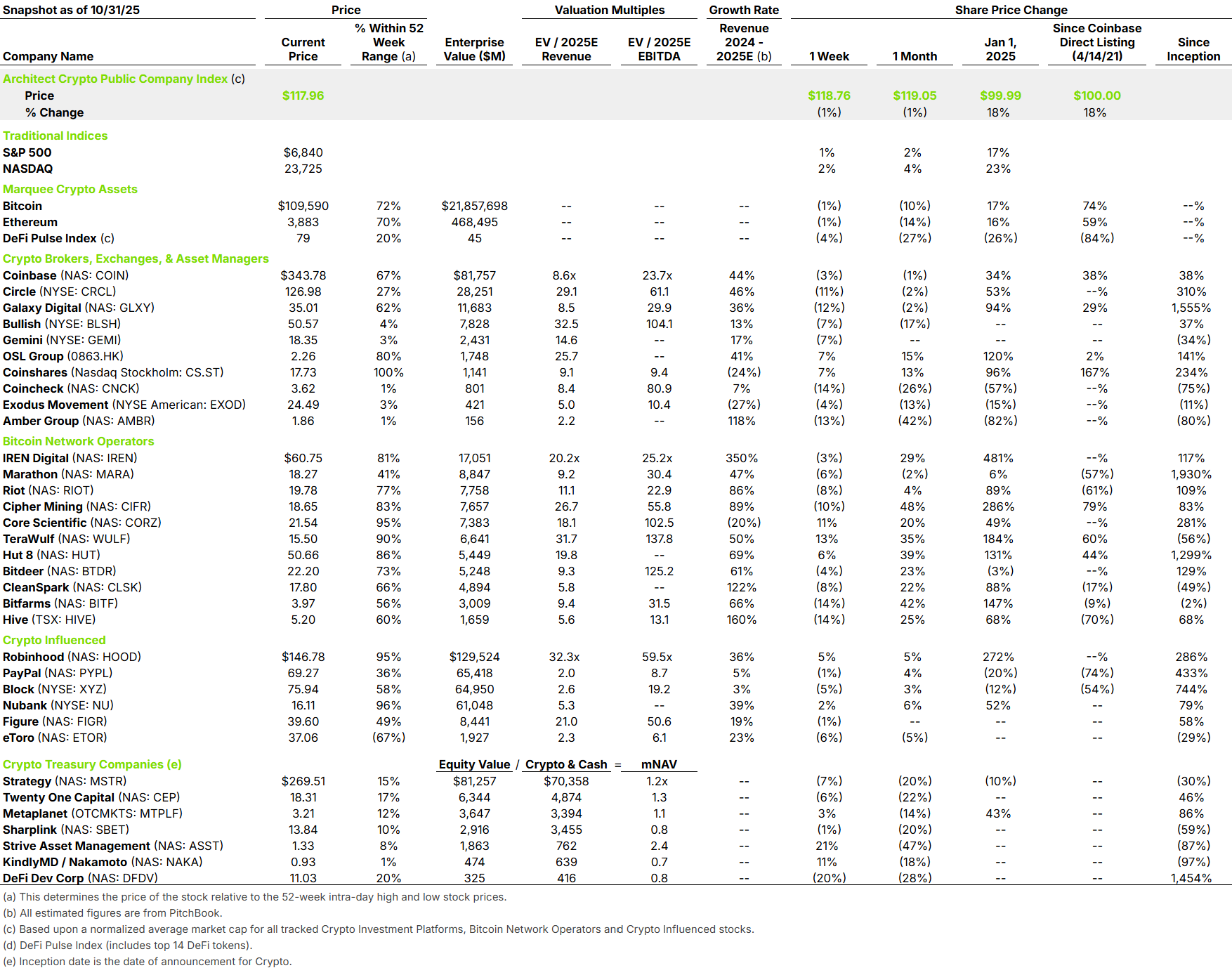

This past week earnings season began with Coinbase, Core Scientific and others making waves. Coinbase’s Q3 2025 was a major success. Revenue was $1.9B (+25% QoQ, +55% YoY), split between $1.0B in transactions (+37% QoQ) and $746.7M in subscriptions and services (+14% QoQ, +34% YoY). Adjusted EBITDA was $801M (+57% QoQ, +78% YoY). Trading volume reached $295B (+24% QoQ) and assets on platform were $516B.

The Deribit deal, closed on August 14, gave Coinbase instant scale in options and perps. It added about $52M to Q3 and helped push institutional transaction revenue to $135M (+122% QoQ) on roughly $236B of institutional volume (+22% QoQ). On a simple day-weighted view, that $52M over 48 days implies roughly $100M of “quarterized” revenue, or about $400M annualized, around Barclays’ $425–$450M 2024 revenue estimate, which frames the purchase at roughly 6.4–7.3x EV to revenue.

This quarter shows the “Everything Exchange” in action. Derivatives and options now sit alongside spot and perps, deepening institutional flow, while about $300B of custody and USDC economics extend monetization beyond trading. Coverage spans roughly 90 percent of crypto market cap, and Coinbase custodies more than 80 percent of U.S. BTC and ETH ETF assets, channeling high-quality assets and clients back to the platform. Net effect: derivatives lift activity and ticket size, custody and ETFs anchor balances, USDC and staking feed subscriptions and services, and together they turn episodic volume into steadier earnings that can support a higher multiple.

On a separate note, Core Scientific shareholders rejected CoreWeave’s approximately $9 billion all-stock acquisition. Shareholders argued that the deal would transfer one of the company’s most compelling growth opportunities to CoreWeave at an unduly low price. The transaction used a fixed-exchange-ratio structure, which does not protect sellers against declines in the acquirer’s share price. One way to address this is a collar (a price-protection mechanism). A collar either fixes the value of the consideration and lets the exchange ratio float within a band (a fixed-value, floating-ratio collar), or fixes the exchange ratio and lets the per-share value vary only within a cap and floor, often with mutual walk-away rights if the band is breached (a fixed-ratio, floating-value collar).