Headlines deserve scrutiny.

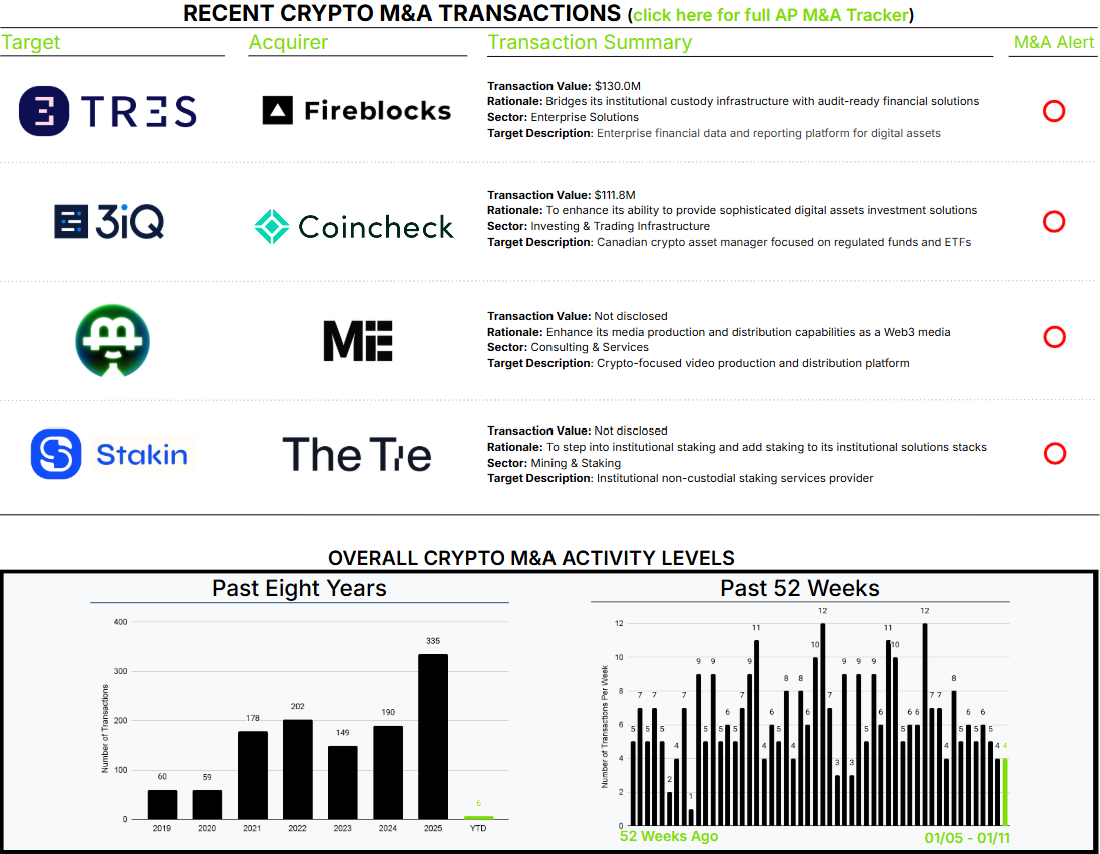

This week Coincheck, publicly traded on the NASDAQ: CNCK, announced the acquisition of 3iQ for total consideration comprised of newly issued Coincheck common stock. The headline value was placed at $111.8M in the press release issued by Coincheck. Coincheck is a Japan-focused crypto brokerage and exchange and 3iQ is a digital asset manager and one of the first issuers of crypto exchange-traded funds (ETFs) and exchange-traded products (ETPs). On the surface, this is quite normal; however, closer assessment reveals several unique elements to this transaction.

First, this is a related-party transaction. Coincheck and 3iQ are both majority owned by Monex Group, a publicly traded Japanese online brokerage firm which owns 84% and 97% of each, respectively. This has important implications for minority shareholders, particularly in the case of Coincheck’s public shareholders.

Second, Coincheck is using its publicly traded common stock as consideration. Again, nothing unusual about this type of structure; however, in this case, 3iQ shareholders (effectively Monex) are accepting a valuation of each Coincheck share of $4.00 when the closing stock price the day before the announcement was $2.66. The headline value of $111.8M (based on the $4.00 price per share) would actually be $72.2M (based on a $2.66 price per share), or 35% lower. What is the “right” calculation of consideration?

This dynamic is common in M&A transactions where publicly traded equity is used as consideration. Stock price can fluctuate substantially during the negotiation, due diligence, and transaction documentation period, which often takes months. One technique to moderate this influence is the use of what is known as volume-weighted average stock price (VWAP) over an agreed-upon time period. In this instance, Coincheck’s 30-day and 60-day VWAP were $5.87 and $5.83, respectively. In addition, when you consider average daily close, the 30-day and 60-day were $3.62 and $3.67. These data points help justify a $4.00 per-share headline value.

Going back to the first topic of related-party transaction issues, one could argue Coincheck’s minority shareholders are advantaged by this circumstance, a good thing. An acquisition that was negotiated to cost $111.8M is actually costing them $72.2M. 3iQ shareholders (again, effectively Monex) could have demanded more shares as the stock price had trended down, but that apparently didn’t happen, benefiting Coincheck rather than 3iQ.

Lastly, Monex acquired its ownership stake in 3iQ in two transactions in April 2024 and September 2025 for an estimated total consideration of $77M.