Stablecoin payments must proliferate.

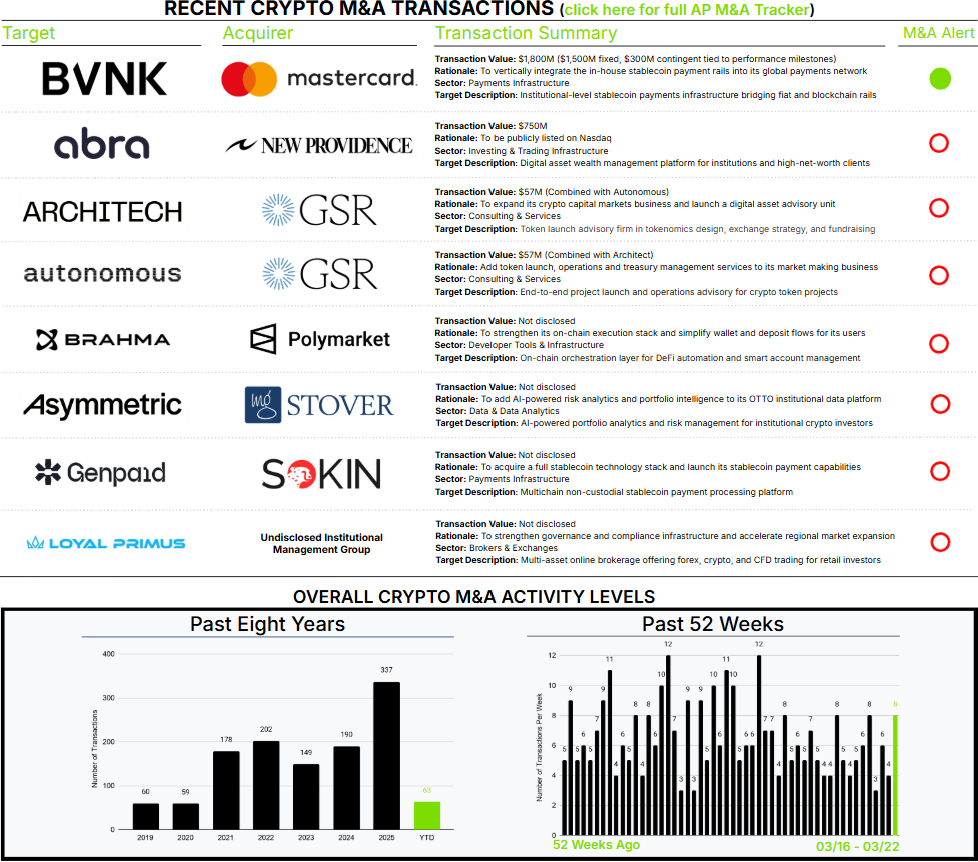

The week’s, and perhaps decade-to-date, headline is Mastercard’s acquisition of BVNK. Mastercard, along with Visa, controls a global network of consumers, merchants, and businesses that rely on and trust its services. Much like Stripe’s acquisition of Bridge 18 months ago, this transaction, along with dozens of non-acquisition initiatives, demonstrates that incumbent payment players have recognized the value proposition of stablecoin-based payments and are embracing it as their own.

As stablecoin usage has expanded beyond crypto trading, the most vexing challenge has become presenting it as an option when a payment is being made or accepted. A simple term we use at Architect Partners is “distribution.” This is what keeps every stablecoin and stablecoin-related payments company up at night. Distribution is exactly what Mastercard, Visa, Stripe, banks, and payment software providers, among others, have to offer.

Now the pressing strategic question begins to shift: if traditional payment players are delivering the missing link, distribution, where does that leave the crypto-native stablecoin-related firms and the L1 and L2 blockchains that created and enabled these new payment rails? Like war, it is hard to predict, but at least the battlefield is now clear.

Far more detail is available in our M&A Alert on the BVNK | Mastercard transaction here, and in our three-part series on Crypto Payments, which we published nine months ago (part I, II, and III).