Bitcoin drawdowns have a distinctive way of showing up in earnings. For companies that hold meaningful crypto on the balance sheet, a BTC decline can shift from a market event to an income statement event through fair value marks, impairment-style charges, and collateral-related impacts.

Two ramifications show up fast.

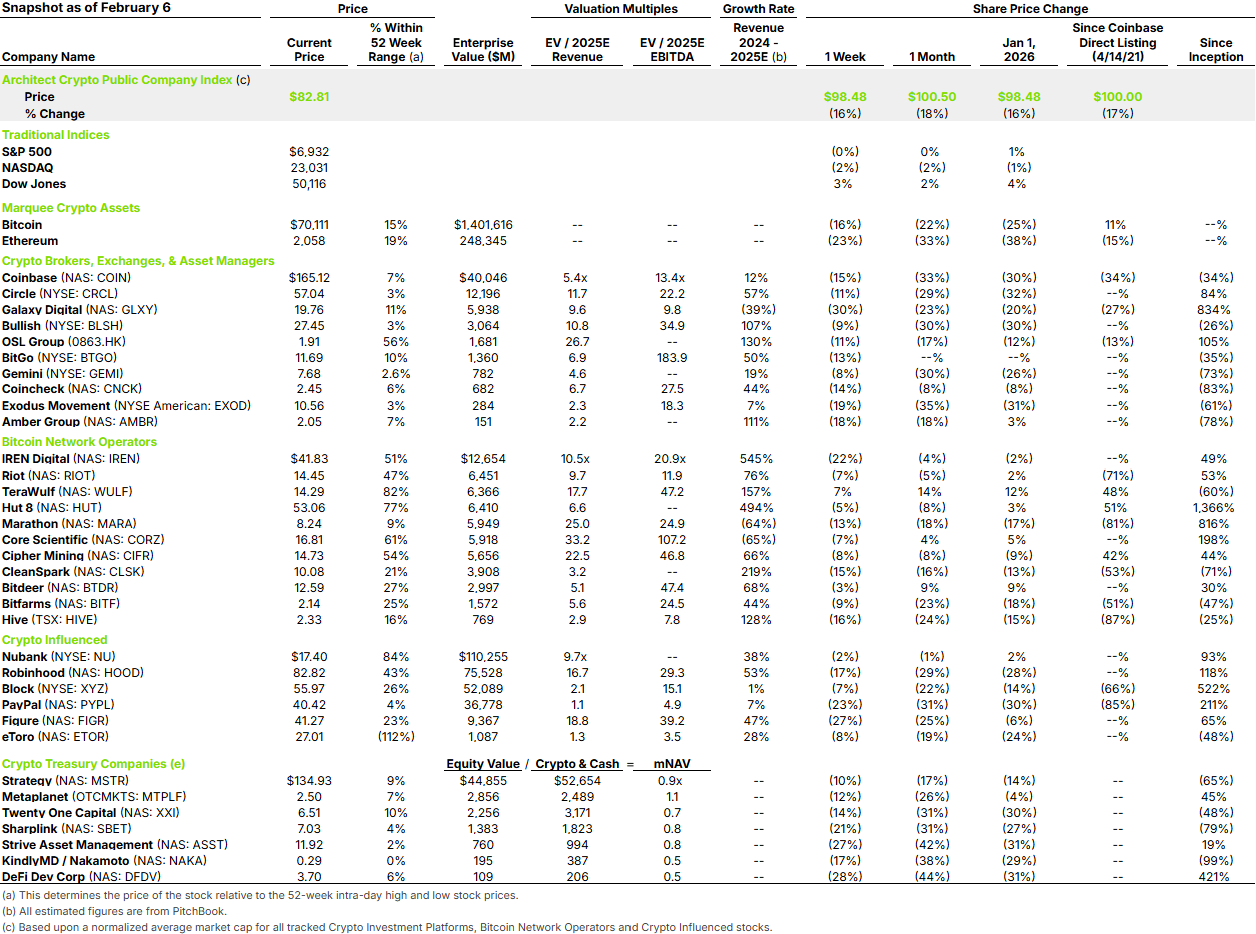

First, accounting optics turn brutal. Even if operations are steady, a big BTC move can dominate the narrative, turning earnings into a referendum on crypto price action rather than fundamentals. Strategy is an extreme example. In Q4 2025, it posted roughly a $12.4B net loss, driven primarily by an unrealized mark-to-market loss on its Bitcoin holdings, not a collapse in fundamentals. These are paper losses, and for most companies they matter mainly insofar as they raise the cost of capital or constrain fundraising (which admittedly is the critical lever for Strategy), not because cash is leaving the business.

Second, collateral and liquidity mechanics can accelerate the downside. Once crypto holdings are connected to financing, a price drop can trigger second-order effects: reduced borrowing capacity, tighter terms, higher haircuts, or the need to post more collateral at the worst time. CleanSpark is a clear illustration. This quarter, it reported a $247M loss on the fair value of bitcoin (net) and a $104M loss tied to bitcoin collateral, showing how declines can hit not just holdings, but also the financing wrapped around them.

This leads to the uncomfortable question: Is BTC a good hedge for corporate balance sheets? A hedge is supposed to reduce stress. Bitcoin’s volatility can do the opposite, especially when correlations rise in risk-off regimes. In the CFO sense, an asset that can move violently does not behave like traditional balance-sheet protection.

But there is a more constructive lens. Bitcoin is often not a hedge, it is a policy choice. The companies that succeed treat it as a high-volatility strategic reserve and design around reality: right-size the position, finance to hold through cycles, keep operating liquidity separate, avoid fragile collateral structures, and communicate clear rules that prevent forced selling.