January 26th – February 1st

PERSPECTIVES by Eric F. Risley

Distribution is king, and the stablecoin proliferation wars have only just begun.

Stablecoins have made their hay as a crypto trading and settlement currency, with impressive success. Today, roughly $300B in stablecoin denominations are outstanding, which earn $14B in annual returns via interest earned on invested reserves. Quite a nice revenue stream for Tether, Circle, Circle’s critically important partner Coinbase, and a smattering of far smaller players. That’s yesterday’s game.

Today, stablecoin growth is, and will continue to be, driven by far more general-purpose use cases. Most notably: payments in many different forms; U.S. dollar denominated savings in countries where local currencies suffer high inflation, capital controls, or confiscation risk; and a wide array of settlement activities outside of crypto trading.

Each of these more general-purpose use cases already has vast ecosystems of corporate, client, and customer participants. These include industries like banking, payments, capital markets, asset management, foreign exchange, specialty finance, corporate treasury management, and trade finance, to name a few. These players currently control access to the customers who will increasingly utilize stablecoins.

Today’s stablecoin leaders have so far largely pursued a strategy of partnership. This offers access to coveted brands, customer relationships, and disparate types of software that manage and orchestrate payment workflows and related processes. Perhaps reasonable, but what inhibits the issuance of company-specific, proprietary stablecoins? Nothing, and it’s already happening.

The acid test may be the answer to this question: Is the form of payment currency the core value proposition of this vast ecosystem of existing participants? We posit no.

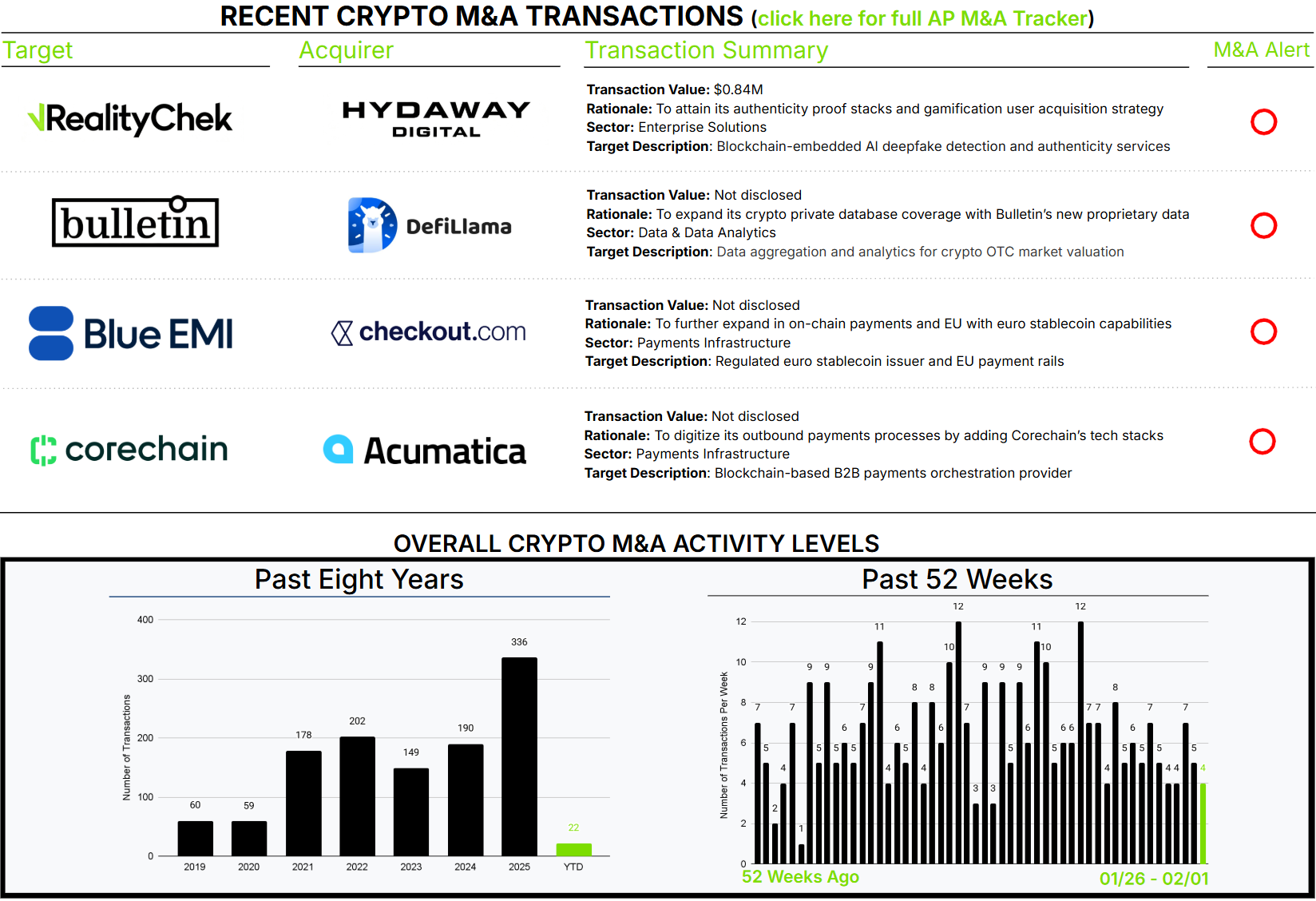

Perhaps the current group of stablecoin players will need to transform themselves from stablecoin issuers into stablecoin-based solutions providers, offering the core value propositions of those they currently seek to partner with. This week, two acquisitions suggest this combination, albeit in reverse form, is the future: traditional payment providers and stablecoins living under the same roof, much like Stripe’s acquisition of Bridge 18 months ago.

We’re looking forward to the coming battles.

See Architect Partners Insights: Crypto Payments & Infrastructure (part I, II, and III) for more information.