April 27 – May 03 (Published May 06th)

PERSPECTIVES by Steve Payne

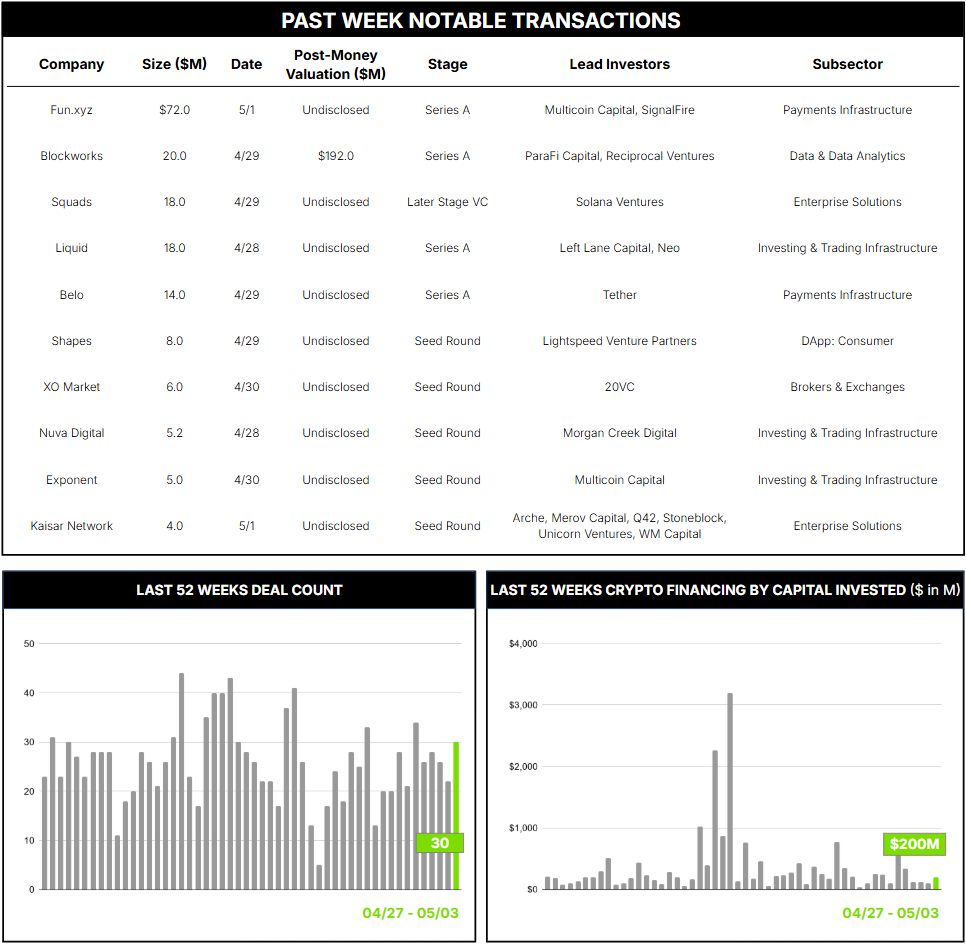

30 Crypto Private Financings Raised: $200M

Rolling 3-Month-Average: $246M

Rolling 52-Week Average: $370M

Announced Deals >$50M: 1

In another relatively slow financing week, blockchain-based payments startup Fun emerged from stealth following the close of a $72 million Series A co-led by Multicoin Capital and SignalFire. The round, which closed in late January, also drew participation from Infinity Ventures, Pharsalus Capital, and Tinder co-founder Justin Mateen. The raise follows a $3.9 million pre-seed led by JAM Fund in 2022, with Nomo Ventures, Great Oaks, and SOMA Capital also participating.

Founded by 26-year-old Stanford dropout Alex Fine, Fun builds the rails for users to move money in and out of platforms, bridging fiat and digital assets without requiring a crypto exchange or bank. The core thesis is simple: at sufficient scale, generic payment infrastructure stops working. Fun processes over $18 billion in transaction volume annually across more than 100 countries, and counts Polymarket, Lighter, and Aave among its roughly 20 clients. It is the sole deposit provider for Polymarket, crypto’s dominant prediction market, where every basis point of conversion translates directly to revenue and user retention.

Fun competes in a crowded field that includes MoonPay, Transak, Ramp Network, and Coinbase Onramp, all of which offer plug-and-play fiat-to-crypto infrastructure. The differentiation is that while competitors sell standardized SDKs, Fun operates as a deliberately small, engineering-led team that embeds directly with client engineers to build custom flows. It seems closer to a specialist systems integrator than an off-the-shelf onramp.

The macro tailwind is real. Meta, Stripe, and Shopify have all added crypto payments over the past year amid a regulatory about-face under the Trump administration. Multicoin GP Spencer Applebaum made the bull case plainly: as fintechs and neobanks worldwide adopt tokens and stablecoins, Fun is positioned to deliver the same bespoke service it provides to crypto-native clients to non-crypto companies over time. Note that this bespoke model may be structurally capacity-constrained, as the same white-glove approach that wins Polymarket could limit how many clients the company can realistically serve.