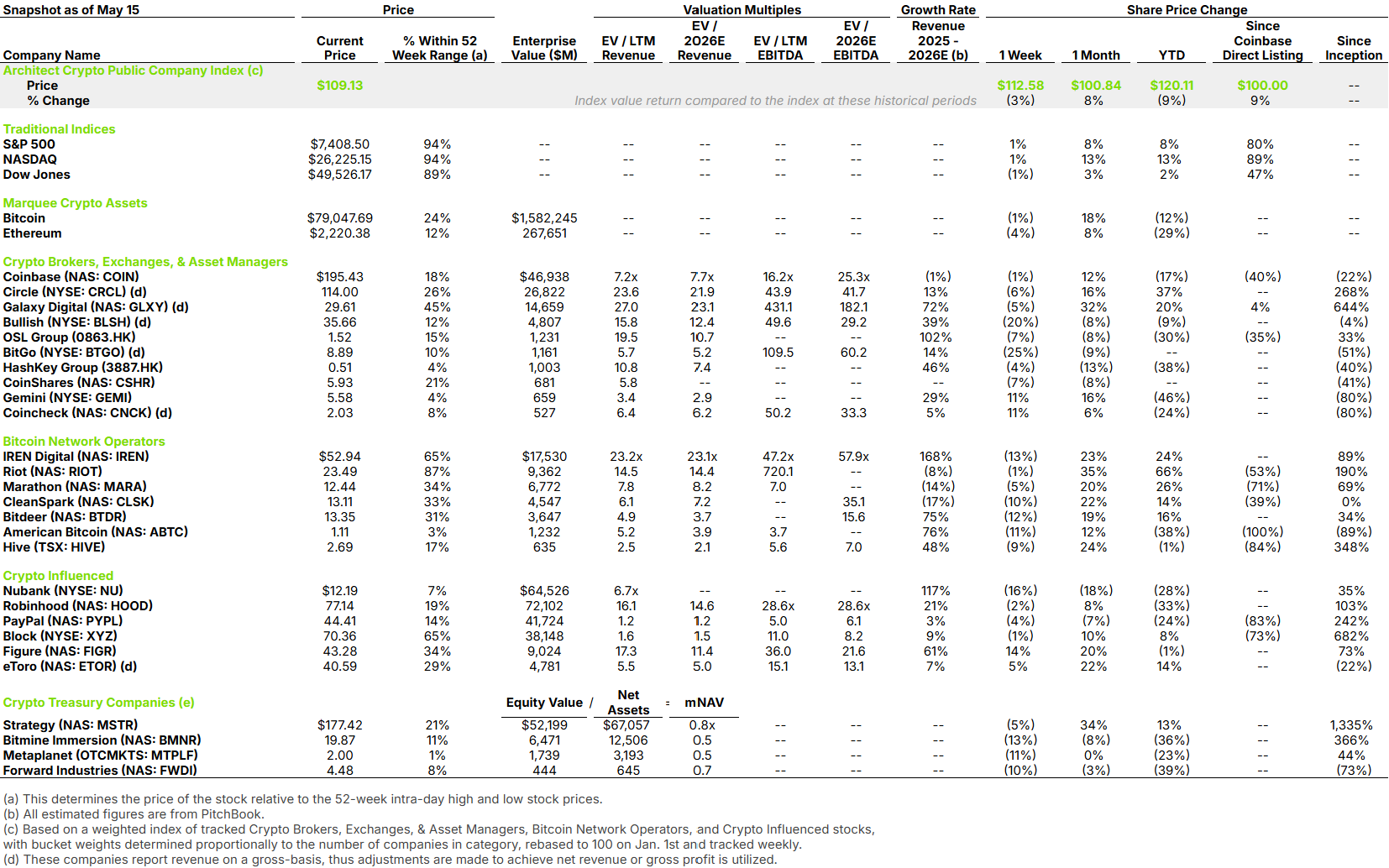

Q1 showed which crypto business models hold up when prices fall and which do not.

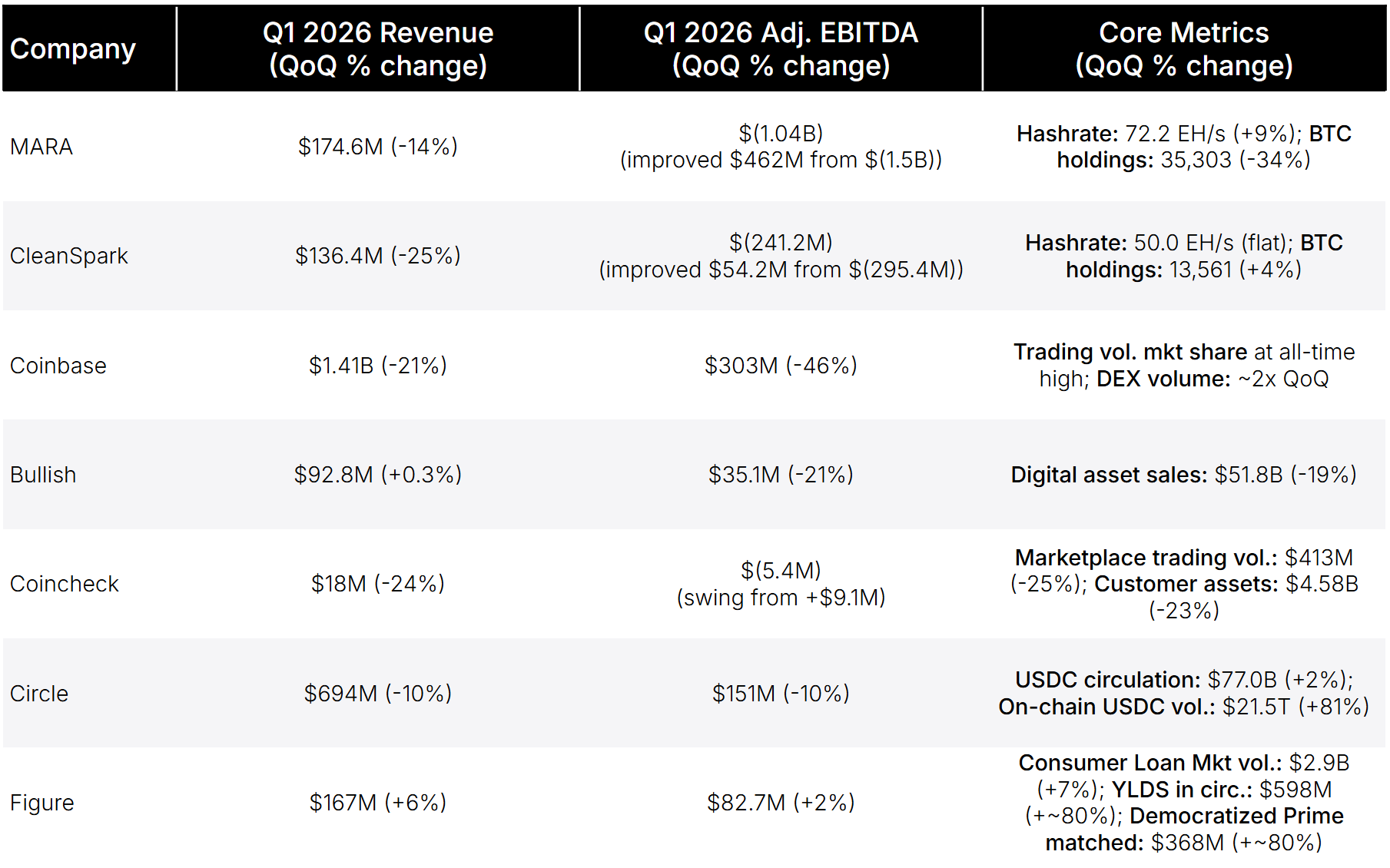

Miners were hit hardest for three reasons. Bitcoin dropped sharply, so each coin mined earned less while energy, hosting, and equipment costs stayed roughly the same (Q1 was predominantly pre-Iran War). Network difficulty stayed high, so unit economics worsened even where output held. Large Bitcoin balances also drove accounting losses through earnings, on top of weaker operating results.

Trading platforms split by customer type. Industry volumes fell as volatility cooled and investors pulled back. Retail-heavy venues took the brunt: Coincheck saw revenue, volume, and customer assets all decline. Coinbase revenue also fell, but it gained market share and doubled DEX volume, showing that despite the down quarter it was faring better than its peers. Bullish, which serves mostly institutional and derivatives clients, held revenue flat as that base kept trading through the quarter: institutional and derivatives flow runs on mandates and hedging rather than the discretionary risk appetite that pulls retail away when prices fall.

Stablecoins and tokenization held up best because their revenue comes from usage, not trading. Circle’s earnings softened on lower interest income, but USDC circulation grew and on-chain transaction volume nearly doubled, showing real payments demand. Figure showed the same pattern, with tokenized consumer credit volume rising and newer products scaling quickly.